Cerebras Just Warned That Its Revenue Growth Will Slow in Q1 2026. The Reason Has Nothing to Do With Demand.

Cerebras put a warning on page 91 of its S-1. The first time the company prints quarterly results as a public company, the number will look worse than the business actually is. Most of the market will read it the wrong way, making this stock a volatile ride over the next few earnings reports.

The warning is one sentence, buried in the section of the filing that nobody reads carefully. [The MD&A. Page 91. Find it.] Here is what the company itself wrote:

“When we begin to recognize contra-revenue amounts from the warrants in the first quarter of 2026, we expect quarterly revenue growth rates will decline from recent trends.”

That is the company telling you, in advance, that the first headline number is going to deceive you.

So what is contra-revenue, and why does it matter so much???

When a company gives a customer a warrant, which is the right to buy stock at a tiny price, accounting rules say that warrant is essentially a discount the customer is earning by doing business with you. You cannot just call it a promotional expense. You have to reduce the revenue you report from that customer by the value of the warrant, spread across the life of the contract. The cash still comes in. The compute still gets delivered. The customer is happy. But the revenue line on the income statement gets shaved down by an accounting entry. That is contra-revenue. It looks like the business is slowing even when it is not. [This is the part that breaks the model in every spreadsheet on Wall Street next quarter.]

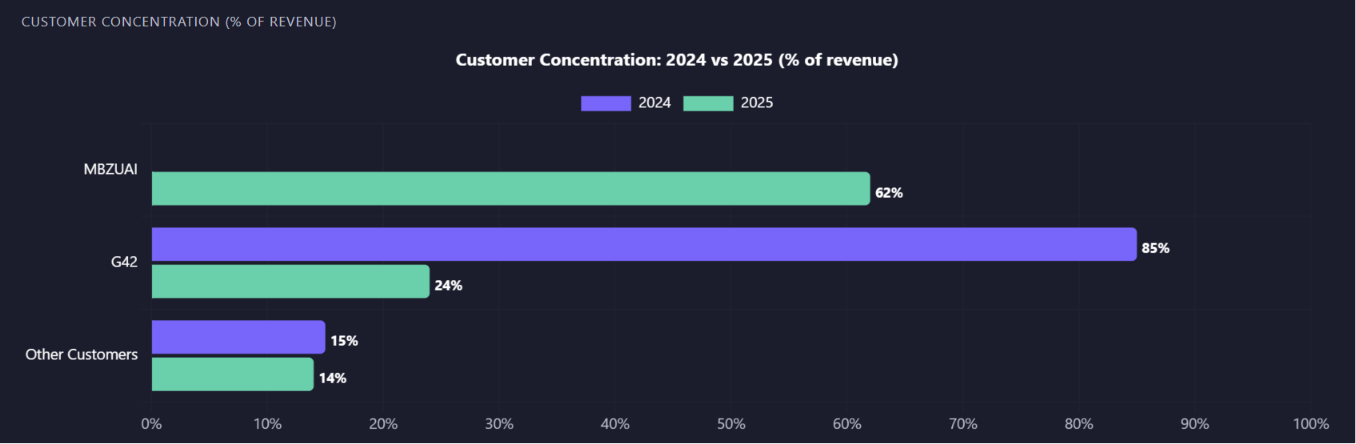

Cerebras has issued warrants to its two biggest customers, and the size of these warrants is not small. G42, which along with its sister organization MBZUAI made up 86% of Cerebras revenue in 2025, was issued a warrant in December 2025 to buy 1,857,516 shares of Class N common stock at a penny each. Fully vested. Exercised in January 2026. A second G42 warrant for 1,655,975 shares followed in April 2026, also at a penny. The customer warrant asset sitting on the balance sheet as of December 31, 2025 was $152.4 million. That entire amount will be drained out of reported revenue between now and October 2031. That is years of headwind to the headline number, and it has nothing to do with how much compute G42 is buying.

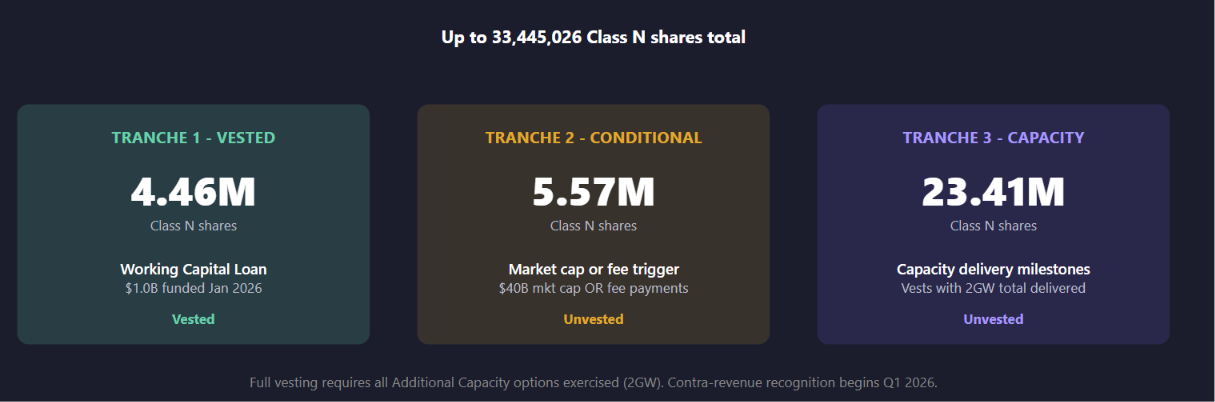

Then there is OpenAI. The OpenAI warrant covers up to 33,445,026 shares of Class N common stock at one one-thousandth of a cent per share. [Yes, the strike price is essentially zero.] As Cerebras ships OpenAI compute and OpenAI hits its milestones, more of that warrant vests, and more contra-revenue flows through. On top of the warrant accounting, the OpenAI deal includes pass-through data center costs. The S-1 says directly that these “will have a dilutive impact on gross margin.” So reported revenue gets pressed down, and the gross margin you see beside it gets pressed down too. Both numbers will look worse than the underlying engine.

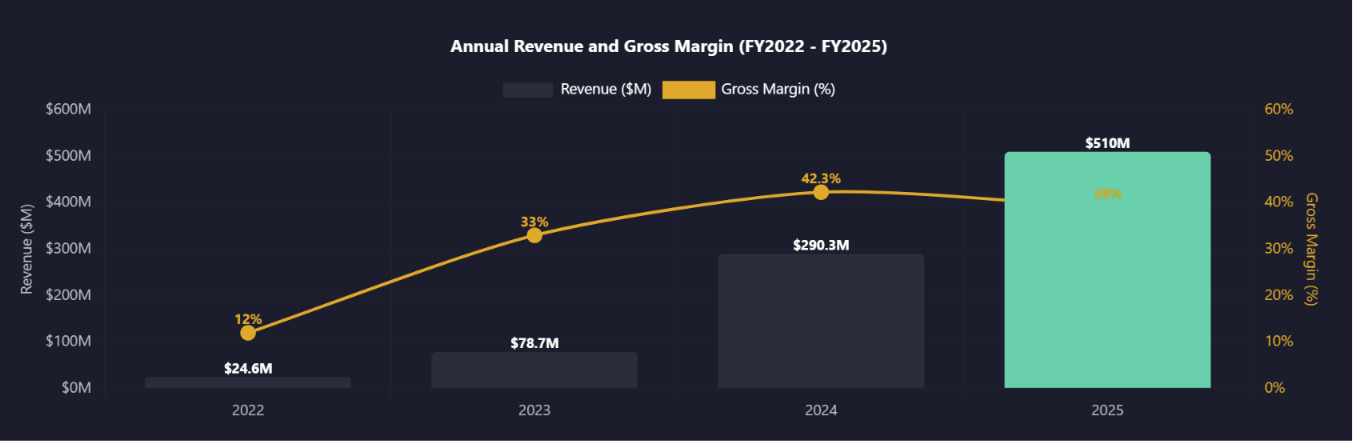

For context on what is actually happening in the business, 2025 revenue was $510 million, up 76% from $290 million in 2024. Hardware grew 69%. Cloud and services grew 94%. Remaining performance obligations, which is the company’s contracted backlog, sits at $24.6 billion.

Here is what to watch and when. The first public quarterly print after Cerebras lists on Nasdaq will probably show reported revenue growth decelerating from the 76% pace of 2025, even though shipments and bookings tell a stronger story. Track non-GAAP, ex-warrant revenue if Cerebras chooses to disclose it. If they do not, you can roughly back into it by adding the warrant amortization disclosed in the footnotes back to reported revenue. Watch the gross margin line carefully. It was 39.0% in 2025, already down from 42.3% in 2024, and pass-through OpenAI data center costs will press it lower from Q1 2026 onward. Watch the mix shift. Cloud and services were 30% of revenue in 2025. That share will rise as OpenAI capacity comes online, because OpenAI is recognized 15% in the first 24 months of the deal, 43% in months 25 through 48, and the balance after. Then take a step back and ask the only question that matters. Is the business growing faster than the contra-revenue is shrinking the headline. If yes, the dip is noise.

Now the honest part. This thesis only works if the OpenAI deal executes on schedule. If Cerebras misses a capacity delivery milestone, OpenAI has the explicit right to terminate part or all of the agreement, and the $1 billion working capital loan from OpenAI becomes immediately due.

The point is simple. The first quarter you see Cerebras report as a public company is not the quarter you are actually looking at. The accounting will be heavier than the business. Most of the market will miss this. You now will not.

If you found this useful, this is the surface.

The full breakdown, including the numbers I’m keeping a closer eye on and what analysts kept pushing on, is inside the What The Chip Happened community.

Join the WTCH community, 33% off at checkout

Institutional-quality semiconductor analysis for serious investors. Deep dives on earnings within 24 hours, conference coverage, and a network of investors who take this seriously.

Get 15% OFF FISCAL.AI — My Favorite Charting Platform —

G42 concentration is the real signal here. When one customer drives over 80 percent of revenue, any timing slip becomes a binary print. Demand is fine, the concentration is the risk factor.

Great article man, actually interesting

Subscribed, would love to have you along too🙂