Micron Earnings Preview: The $35 Billion Question

What Wall Street wants, what management has signaled, and the three numbers that decide how MU trades on Wednesday

Micron (MU) reports fiscal Q3 2026 on Wednesday, June 24, after the close. This is not a normal memory print. The company is about to report a single quarter that exceeds its entire annual revenue for every fiscal year through 2024.

Here is the one-sentence setup. The beat is already priced in, so the stock will trade on the guide, the 2027 high-bandwidth memory commentary, and whether an 81 percent gross margin can hold.

Let me walk through it the way I would brief it.

The bar Micron set, and the bar the Street raised

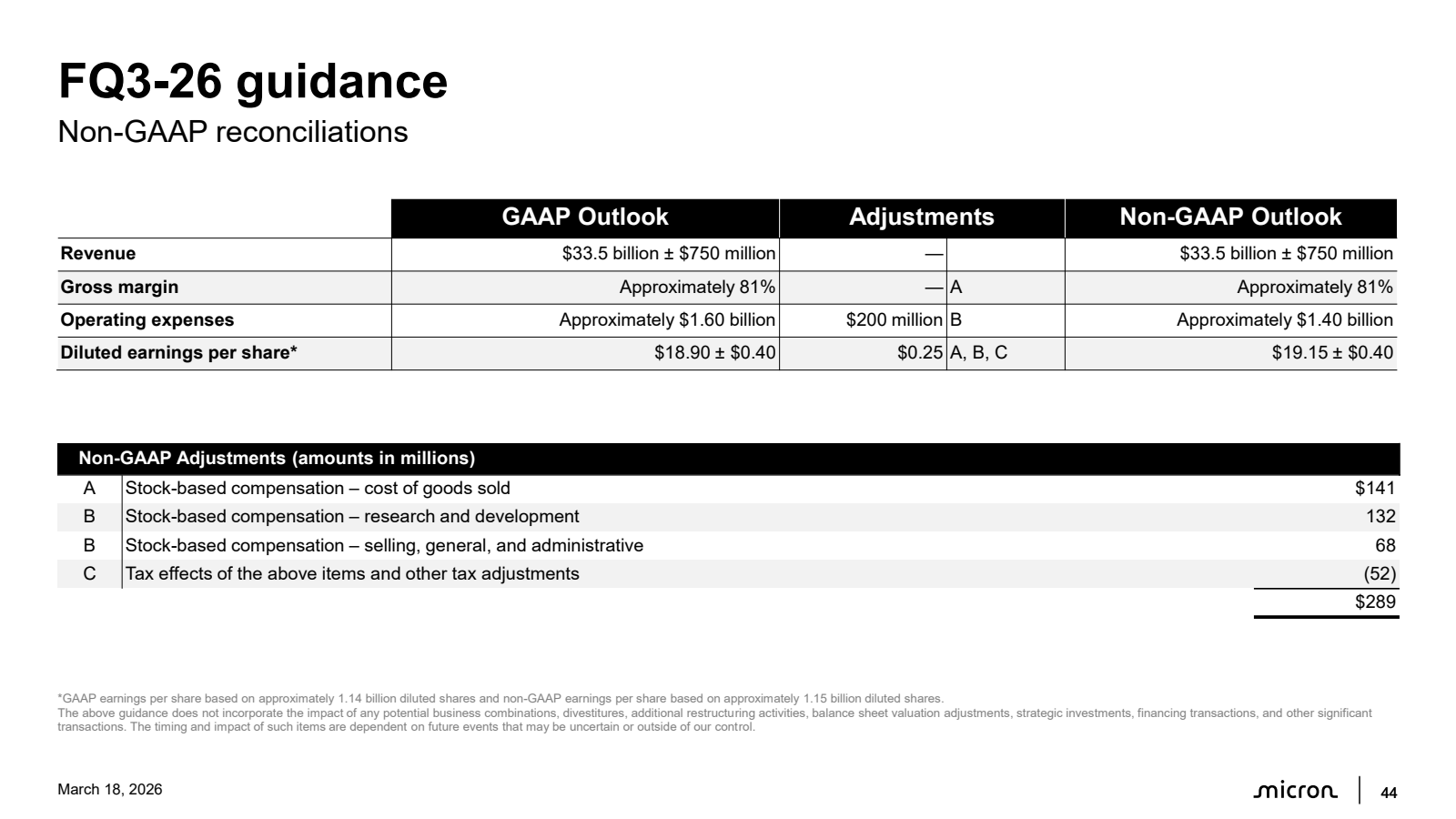

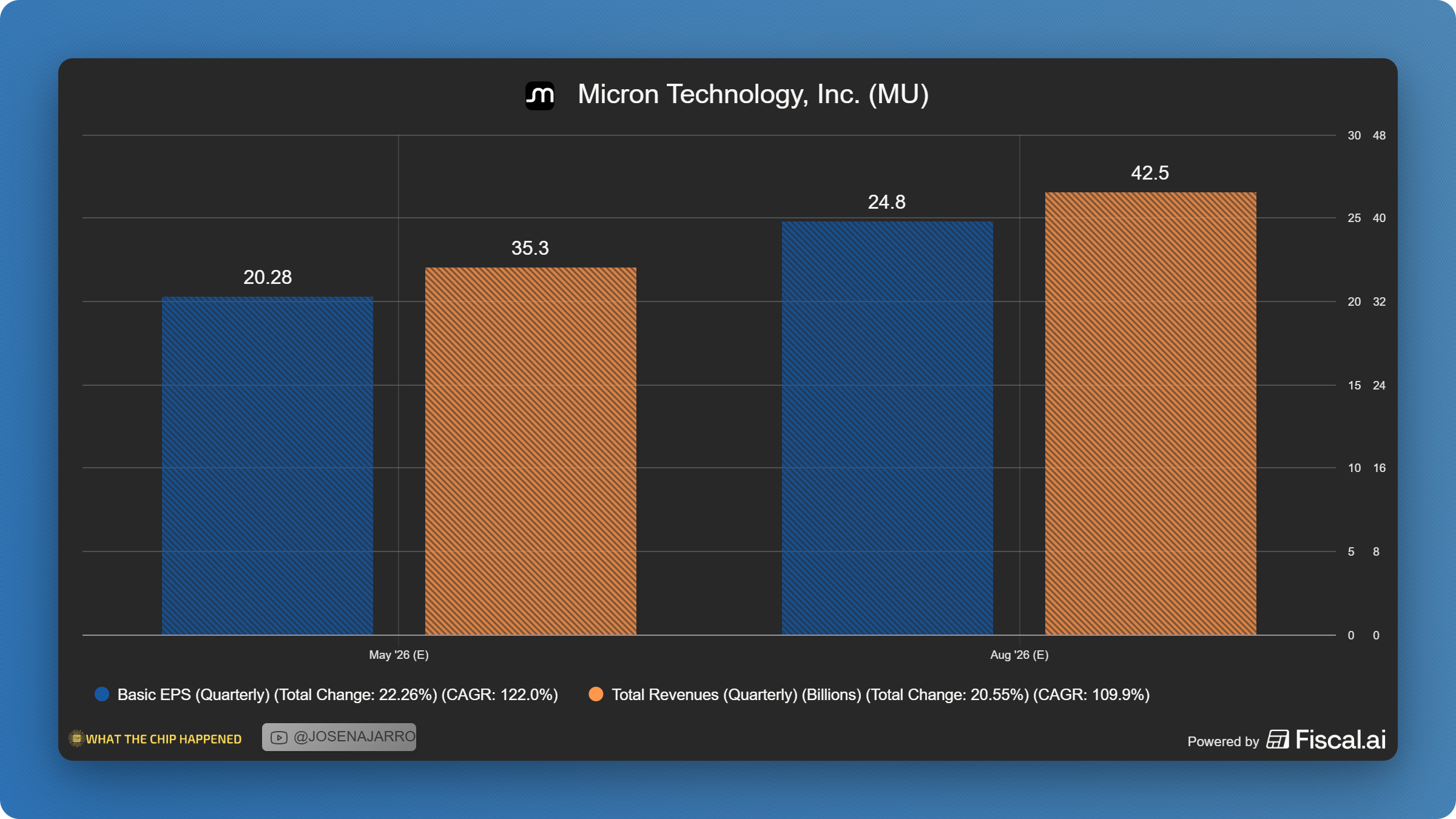

Back in March, Micron guided fiscal Q3 to record revenue of $33.5 billion (plus or minus $750 million), gross margin of around 81%, operating expenses near $1.4 billion, and non-GAAP EPS of $ 19.15 (plus or minus $0.40) on roughly 1.15 billion shares.

The Street did not stop at the guide. Consensus has climbed to roughly $35 billion in revenue and $20 in EPS, with gross margin near 81.6%. That revenue figure sits more than a billion dollars above Micron’s own midpoint.

What that means for investors: a guidance beat alone may not be enough. If Micron simply meets the Street at $35 billion, it will have beaten its own March guide by nearly $1.5 billion in a single quarter, and the market will still ask, “what’s next.” That is the danger of a stock that has already run.

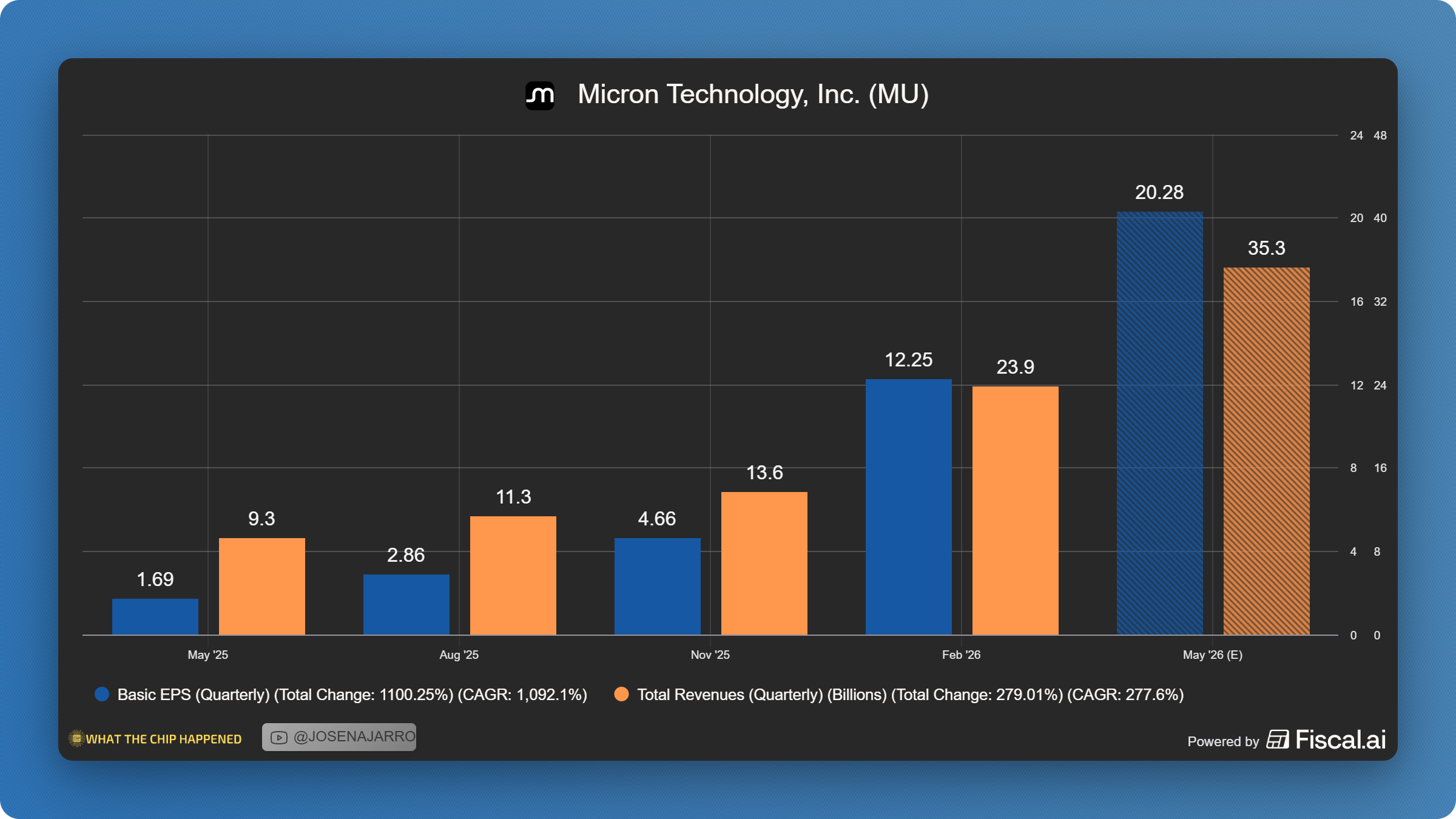

The growth math is staggering on any base. Against a year ago, consensus revenue implies roughly 270-283% year-over-year growth (off about $9.3 billion in Q3 FY2025), and EPS growth above 900% (off 1.91). Sequentially, that is about 47% revenue growth from last quarter’s $23.9 billion, and roughly 60-65% EPS growth from $ 12.20.

Why last quarter matters: the slope, not just the number

Fiscal Q2 is the foundation every analyst is building on.

Revenue was $23.9 billion, up 196% year over year and up 75% sequentially. The $10.2 billion sequential increase was the largest in company history. It was the fourth consecutive quarterly revenue record.

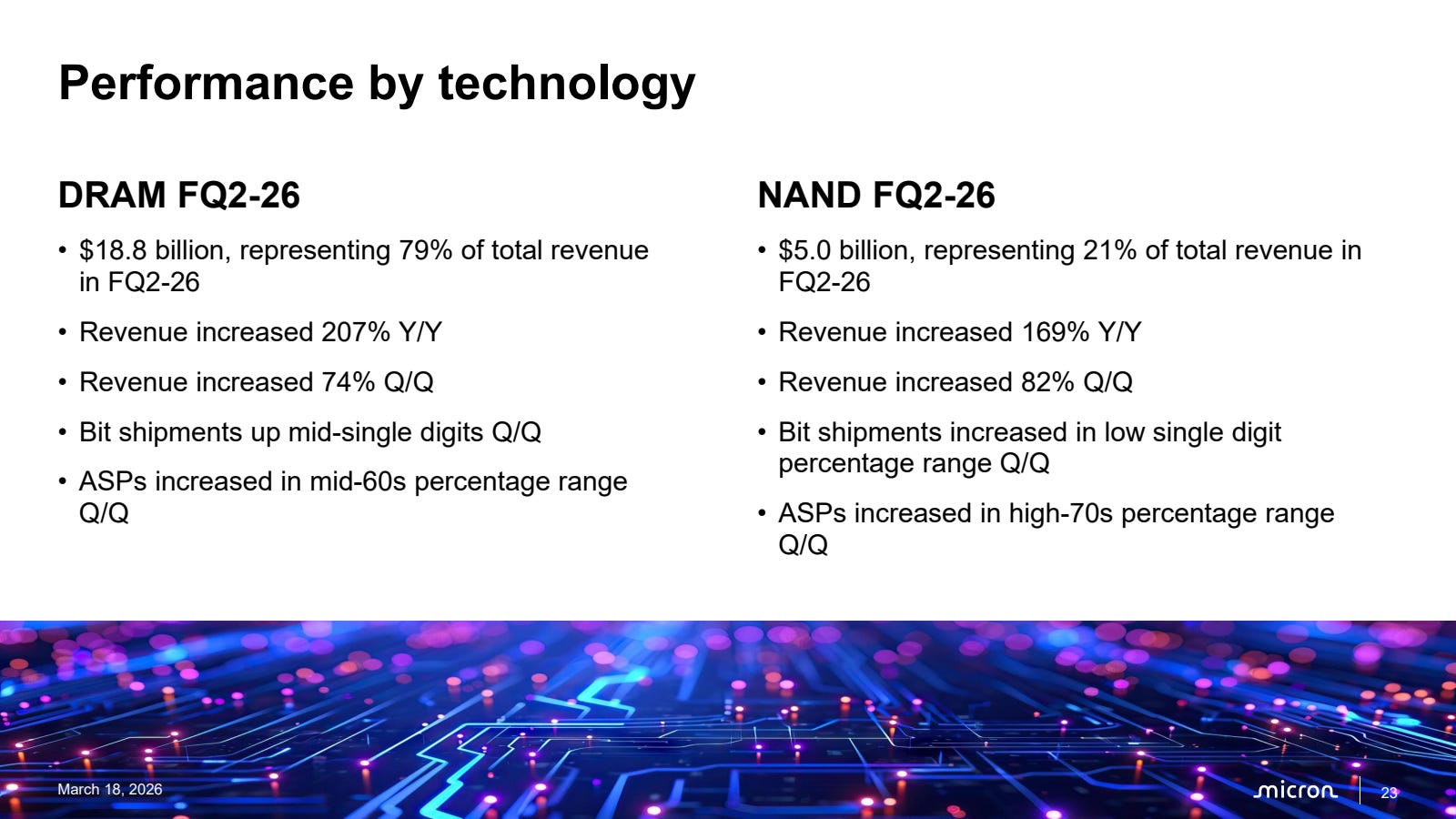

DRAM did the heavy lifting. DRAM revenue was a record $18.8 billion, which is 79% of total company revenue, up 207% year over year. DRAM prices rose in the mid-60 percent range quarter over quarter. NAND revenue was $5 billion, up 169%, with prices up in the high-70s.

Company gross margin came in at 75%, nearly double the prior year. Free cash flow was a record $6.9 billion, and Micron closed the quarter at its strongest net cash position ever at $6.5 billion. The board raised the dividend 30% to $0.15.

What that means for investors: the entire bull case rests on whether this pricing curve is still accelerating. The single most important data point on Wednesday is the quarter-over-quarter pricing cadence in DRAM.

This is the free preview. Inside the WTCH community, you get exclusive live streams, deep-dive reports, full earnings breakdowns, and courses. Join here.

The 81 percent gross margin debate

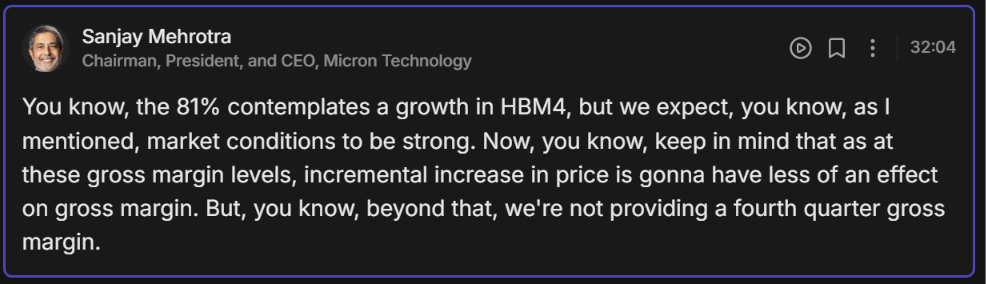

If Micron achieves an 81% gross margin, it will be an all-time company record. Prior memory peaks topped out in the low 60s. So the most-asked question on the Street is whether this is the top.

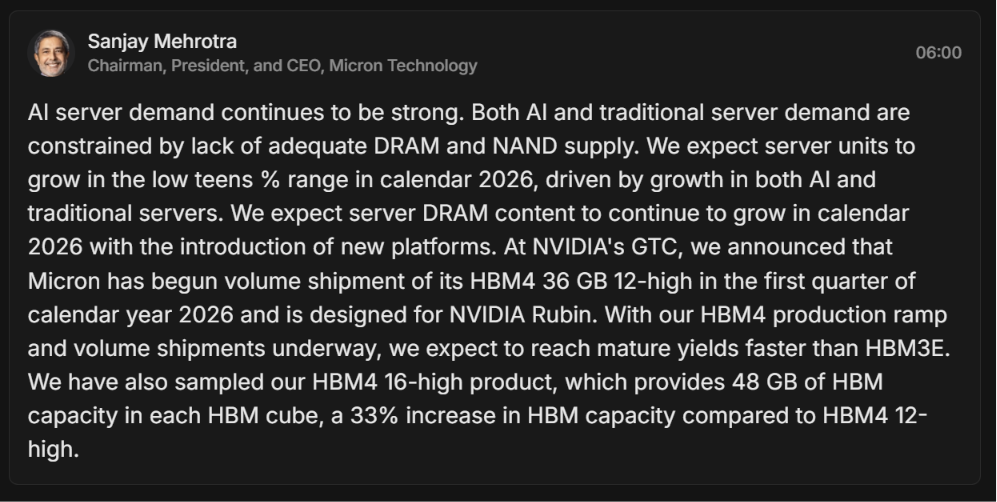

Management’s framing is honest about the math. The CEO has noted that at these margin levels, incremental price increases add less to the margin than they did at lower levels. HBM4 also carries lower margins today than standard DRAM, so as HBM4 scales, mix becomes something to monitor rather than ignore.

There is an underappreciated offset, though. On the Q2 call, Micron’s chief business officer said non-HBM DRAM margins, both inside and outside the data center, have at times exceeded HBM margins. Investors have fixated on HBM as the only pricing-power story. The standard, “boring” DRAM book is quietly one of the strongest margin contributors Micron has.

One crucial point for investors to note is that Micron must maintain a good balance between HBM and Server DRAM, because if you only make HBM, you will have tons of AI accelerators but no AI servers to use them. So the balance from Micron and other leading memory players is crucial!

What that means for investors: do not read the Q4 gross margin commentary as a single number. Read it as a signal. Management declined to guide Q4 margin in March. If they hint at expansion or even stability beyond Q3, the peak-margin fear loses its teeth.

The guide and the 2027 HBM question

This is where the stock actually moves.

The Q4 revenue guide is the headline. The Street reportedly wants it above the $40 billion range. Land inside or above that, and the bulls get their confirmation that sequential acceleration continues into the August quarter. Land below, and the reaction gets ugly regardless of how clean the Q3 print is.

The second forward catalyst is 2027 HBM allocation. Micron’s full calendar 2026 high-bandwidth memory supply is already sold out. At the May J.P. Morgan conference, EVP of Global Operations Manish Bhatia would not confirm 2027 is locked, noting only that they secured 2026 a year early and that they are not commenting on 2027 HBM yet. A statement that 2027 is committed would be the most bullish thing management could say on Wednesday.

The product engine supports it. HBM4 is ramping at roughly twice the pace of HBM3E 12-high, shipping into NVIDIA’s (NVDA) Vera Rubin platform since March, with yields coming up faster than the prior generation. The next inflection, HBM4E, ramps in calendar 2027 on the 1-gamma node, with the first product being a JEDEC-standard part and TSMC (TSM) supplying the logic base die.

One stat frames the entire supply story. Micron has said it can fill only 50 percent to two-thirds of customer demand in the medium term. If that gap holds or widens on Wednesday, pricing power runs longer than a normal cycle would allow.

What analysts kept pushing on

Throughout the Q2 call and the spring conferences, three lines of questioning recurred.

First, the Strategic Customer Agreements. Micron signed its first five-year SCA with a large customer and says it is in talks with multiple others across multiple markets. These are multi-year volume commitments, a structural change from the old one-year LTAs. Analysts want to know how many are now signed and how much of forward bit supply they cover. Notably, this is the opposite approach to SK Hynix and Samsung, who have reportedly been rejecting multi-year agreements to ride quarterly price step-ups.

Second, margin durability through the cycle. Analysts repeatedly tried to get management to confirm a floor mechanism inside the SCAs that would protect margins on the other side of the cycle. Management would not confirm specifics, citing confidentiality, but kept repeating that conditions stay tight beyond calendar 2026.

Third, the cash. Micron could exit the calendar year with more than $50 billion in cash. With CHIPS Act restrictions limiting buybacks, the capital-return path is the dividend plus opportunistic repurchases, while the balance sheet keeps deleveraging. The company received credit upgrades from all three agencies this year.

The wildcard: the Anthropic deal

One day before earnings, Micron announced a strategic agreement with Anthropic, the maker of Claude.

The deal bundles three things. A memory and storage supply agreement covering Micron’s data center portfolio of high-bandwidth memory, DRAM, and SSDs. A strategic investment by Micron into Anthropic’s Series H round. And internal adoption of Claude across Micron’s engineering and operations teams.

Anthropic confidentially filed for a U.S. IPO on June 1, after raising 65 billion dollars in a Series H that valued it at 965 billion. Anthropic’s compute chief framed the rationale plainly, saying memory and storage are central to how efficiently they train and serve Claude.

What that means for investors: the timing is deliberate. Micron added a named frontier-AI buyer to its demand story 24 hours before it has to defend that story on a call. It also fits the SCA pattern of locking large customers into multi-year, vertically-integrated supply relationships. Expect management to reference it.

The market backdrop

The macro setup supports the bulls. On the supply side, new greenfield fab capacity does not arrive in meaningful volume until 2027 and 2028. Micron’s Idaho 1 fab produces its first wafers in mid-2027, the Tongluo site in Taiwan ramps up in late 2027 and into 2028, and the new Singapore NAND fab starts in the second half of 2028.

How I am watching it

The Q3 print is the easy part. Revenue near $35 billion and EPS near $20 is the base case. The reaction lives somewhere else.

Watch the Q4 guide. Watch for any statement that 2027 HBM is committed. Watch whether 81% gross margin holds or expands. Those three answers decide whether Wednesday’s roughly 14 percent implied move resolves up or down.

If this is how you like to read the market, the rest is inside.

Most of the research I do never makes it to the free list. The full earnings and conference breakdowns, the companies I am tracking across chips, memory, equipment, and AI infrastructure, and the analysis I use to make my own decisions all live in the What The Chip Happened community. It is built for people who take semiconductor investing seriously and want the work done.

Join here: whatthechiphappened.com

Not investment advice. Do your own research. Figures sourced from Micron’s fiscal Q2 2026 earnings call, the February 2026 Wolfe Research conference, the May 2026 J.P. Morgan conference, company guidance, and Street consensus as of June 23, 2026.