Supply Chains Scream While Demand Explodes: Intel Starves, TSMC Doubles Down, Intuitive Plays Defense

Welcome, AI & Semiconductor Investors,

The earnings confessionals this week revealed an industry grappling with a problem most would kill for: demand so strong it's breaking supply chains. Intel's data center business grew 15% QoQ but warned Q1 revenue will crater 11% because they literally can't make enough chips. TSMC's CEO spent his earnings call validating hyperscaler bank accounts and just committed $56B in CapEx because silicon is the bottleneck. Meanwhile, Intuitive Surgical proved it can print $2.5B in free cash flow while nervously eyeing six different macro threats. — Let's Chip In.

What The Chip Happened?

🏭 Intel’s Data Center Surge Hits a Brick Wall Made of Wafers

🚀 TSMC CEO Does Due Diligence on Hyperscaler Wealth, Likes What He Sees

🤖 Intuitive’s 20 Million Patient Victory Lap Gets Interrupted by Reality

Read time: 7 minutes

Join WhatTheChipHappened Community — 33% OFF Annual Use Code “2026”

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

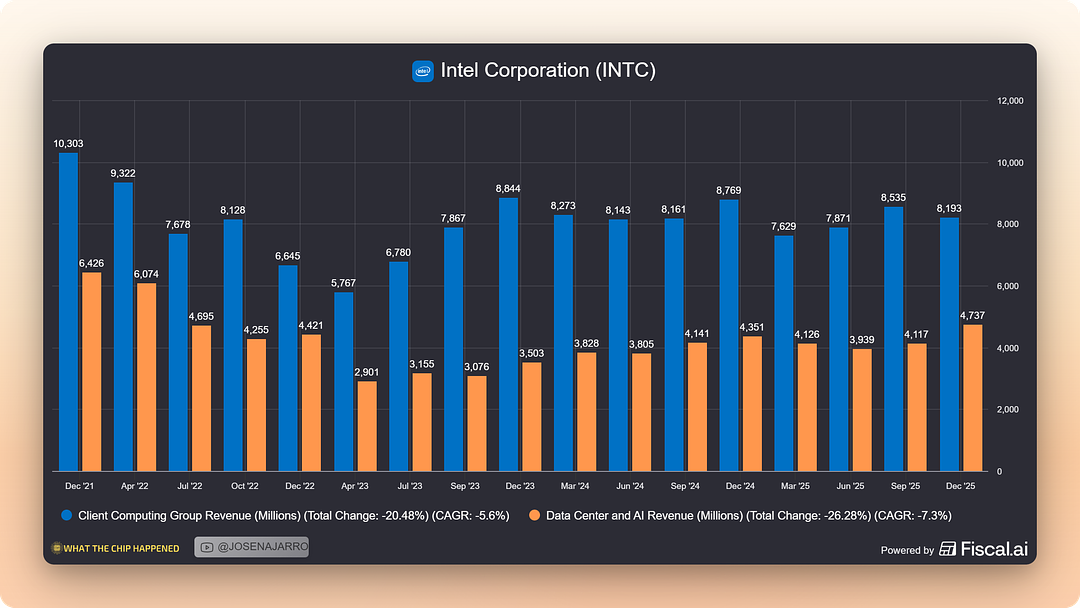

Intel Corporation (NASDAQ: INTC)

🏭 Intel’s Data Center Boom Hits Supply Wall — Q1 Revenue Dropping 11%

What The Chip: Intel just posted its fifth consecutive quarter of beating guidance with Q4 revenue hitting $13.7B, but the celebration lasted about as long as their buffer inventory. The company warned that severe supply constraints will hammer Q1 2026 results to just $12.2B at midpoint—an 11% sequential nosedive. The cruel irony: their Data Center and AI business is growing at the fastest pace this decade with 15% QoQ growth, and management flat-out admitted revenue “would have been meaningfully higher” if they could actually manufacture enough chips. Oh, and they just became the only company on Earth shipping gate-all-around transistors with backside power at volume with their Intel 18A process.

Details:

⚡ Data Center Inflection is Real: DCAI revenue hit $4.7B, up 15% QoQ and 9% YoY—the fastest sequential growth Intel has seen in over ten years. Management confirmed they’re supply-constrained in this segment, which validates the bull thesis that Intel’s AI CPUs actually matter in the data center buildout.

🚩 Q1 Guide is Brutal: Revenue guided to $11.7B-$12.7B ($12.2B midpoint) as internal supply constraints hit peak pain. Buffer inventory has been depleted, and the wafer mix shift toward servers that started in Q3 won’t emerge from fabs until late Q1. Gross margin collapses to 34.5% with EPS at breakeven ($0.00 non-GAAP).

🎯 18A Milestone Delivers: Intel shipped its first Intel 18A products with Core Ultra Series 3 (Panther Lake), launching 3 SKUs versus the 1 SKU commitment. This makes Intel the only manufacturer globally shipping GAA transistors with backside power delivery at volume—a genuine technology leadership moment that’s being overshadowed by near-term supply pain.

💰 ASIC Business Crosses $1B: The custom ASIC business grew 50%+ in 2025 and hit a $1B+ annualized run rate in Q4. Intel is positioning this against a $100B TAM opportunity, suggesting Foundry is gaining traction beyond the headline-grabbing hyperscaler deals.

📉 Margin Reality Check: That 34.5% Q1 gross margin isn’t just supply mix—Panther Lake is actively dilutive to margins right now. CFO David Zinsner admitted this level is “by no means acceptable” and set 40% as the first recovery milestone before they’ll set a higher target. Translation: yield issues are real.

💡 Cost Cuts are Working: Non-GAAP OpEx fell 15% YoY to $16.5B as headcount dropped from 108.9K to 85.1K employees. Intel is targeting $16B OpEx for full year 2026, showing restructuring discipline while navigating the supply crisis.

🛡️ Balance Sheet Fortified: Intel exited 2025 with $37.4B in cash and investments after closing NVIDIA’s $5B equity investment, completing the Altera sale, and securing government funding. The liquidity crisis narrative is dead—they have runway to execute through this rough patch.

⚠️ Industry Component Shortage: Intel warned that DRAM, NAND, and substrate shortages are hitting the entire industry, which could pressure client margins and “limit our revenue opportunity this year.” The supply chain crunch extends beyond Intel’s internal fab constraints.

📈 Client Business Struggles: CCG revenue declined 7% YoY despite AI PC units growing 16%, pointing to significant ASP pressure in the consumer segment. Management is targeting 45% client market share “over the next several years”—an admission they’ve lost share and need multiple years to recover.

🔮 The Coordinating CPU Thesis: CFO Zinsner laid out Intel’s long-term bull case: “The world is shifting from human prompted requests to persistent and recursive commands driven by computer-to-computer interactions.” Intel believes the CPU’s role coordinating AI agent traffic will drive both traditional refresh and entirely new demand vectors.

Why AI/Semiconductor Investors Should Care: This is what genuine AI-driven demand inflection looks like—growing so fast you can’t manufacture enough to capture it. The Q1 guide is ugly, but it’s a supply problem not a demand problem, and those tend to be fixable with capital and time. The 18A milestone validates Intel’s process technology comeback story, but the 34.5% gross margin reveals the cost of ramping new nodes. Bulls should watch for evidence of Q2 supply improvement and Panther Lake yield trajectory—if Intel executes, there’s significant pent-up revenue waiting to be captured in DCAI. Bears will rightfully focus on the path from 34.5% to 40%+ margins, which remains dependent on yield improvements that haven’t been quantified yet. Intel 14A customer announcements expected H2 2026 to H1 2027 will be the next validation point for Foundry credibility.

Join WhatTheChipHappened Community — 33% OFF Annual Use Code “2026”

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

Taiwan Semiconductor Manufacturing (NYSE: TSM)

🚀 TSMC CEO Checks Hyperscaler Bank Accounts, Then Commits $56B

What The Chip: TSMC’s CEO C.C. Wei did something remarkable on the Q4 earnings call: he admitted he was “nervous” about committing $52-56B in 2026 CapEx, so he personally validated AI demand with every major hyperscaler. His conclusion after reviewing their financials? “They are very rich.” The company delivered 62.3% gross margins (beating guidance by 130bps), raised its 5-year AI accelerator revenue CAGR forecast to the mid-to-high 50s%, and warned that supply will remain constrained through 2027 despite the massive capital deployment. Translation: the AI infrastructure buildout is real, it’s massive, and TSMC has line-of-sight that few others possess.

Details:

💰 Q4 Crushed Expectations: Revenue hit $33.7B (+5.7% QoQ in NT$ terms) with gross margins at 62.3%—130bps above the high end of guidance. Operating margin reached 54% driven by cost improvements and high utilization rates. Full year 2025 revenue hit $122B, up 35.9% YoY.

🤖 AI Revenue Trajectory: AI accelerators reached “high teens %” of total 2025 revenue, with the entire HPC platform now representing 58% of revenue (+48% YoY). TSMC raised its 2024-2029 AI accelerator CAGR forecast to mid-to-high 50s%—a breathtaking growth rate sustained over five years.

⚡ Advanced Nodes Dominate: 77% of Q4 wafer revenue came from 7nm and below, up from 69% in 2024. The 3nm node alone contributed 28% of wafer revenue as N2 entered high-volume manufacturing in Q4 with “good yield” at both Hsinchu and Kaohsiung sites.

🏭 Unprecedented CapEx Commitment: 2026 budget of $52-56B (up from $40.9B in 2025), with the next 3 years “significantly higher” than the prior 3 years’ $101B combined total. TSMC is betting $150B+ that AI demand sustains, making this one of the largest capital commitments in semiconductor history.

🔥 Supply Stays Tight Through 2027: Despite the massive CapEx, CEO Wei confirmed capacity constraints will persist through 2026-2027. His message to investors: “We have to work extremely hard to narrow the gap.” Hyperscalers told him silicon from TSMC is the bottleneck, not power or infrastructure.

🌍 Arizona Expansion Accelerates: Fab 1 is in high-volume production, Fab 2 has been pulled forward to H2 2027 (from 2028), Fab 3 construction has started, Fab 4 permits are underway, and TSMC just purchased a second land parcel in Arizona. This is what conviction looks like in physical form.

📈 Monster 2026 Guidance: Revenue growth guided to ~30% YoY with Q1 revenue at $35.2B midpoint (+38% YoY). Gross margins guided to 63-65% for Q1, with long-term framework targeting 56%+ gross margins through the cycle despite margin headwinds from new nodes and overseas fabs.

🎯 CEO Did His Homework: Wei spent “a lot of time” talking to customers and end customers. He checked hyperscaler financials personally and confirmed they’re investing in power infrastructure 5-6 years ahead of silicon needs. His takeaway: “AI really helps their business. They grow their business successfully and healthy in their financial return.”

💡 Dividend Boost Signals Confidence: 2026 dividend guided to at least TWD 23/share versus TWD 18 in 2025—a 28% increase that shows TSMC can fund massive CapEx while returning more cash to shareholders.

⚠️ Margin Headwinds Acknowledged: N2 ramp creates 2-3% gross margin dilution while overseas fabs add 2-4% dilution. However, N3 is expected to cross above corporate average margins “sometime in 2026,” showing the path to absorbing new node costs.

Why AI/Semiconductor Investors Should Care: TSMC just gave investors unprecedented demand visibility backed by CEO-level validation of hyperscaler financials and infrastructure planning. When the world’s leading foundry commits $150B+ over three years and still expects supply constraints through 2027, that’s a signal the AI infrastructure buildout is structurally larger than most models anticipate. The combination of 25% overall revenue CAGR, 50%+ CAGR for AI accelerators, 56%+ target gross margins, and technology leadership with N2/A16 creates a multi-year compounding story. The risk is execution—$150B is enormous capital at risk if AI demand disappoints, and Wei’s admission of being “nervous” shows management understands the stakes. But his due diligence on customer financials and power infrastructure planning suggests downside risk is limited. Watch for N3 margin crossover timing in 2026 and whether Q1 gross margins hit the 64% midpoint—those will validate whether TSMC can maintain margin discipline while ramping capacity aggressively. This is the purest AI infrastructure play available to public market investors.

Join WhatTheChipHappened Community — 33% OFF Annual Use Code “2026”

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

Intuitive Surgical (NASDAQ: ISRG)

🤖 Intuitive Hits 20M Patients, Then Lists Six Reasons to Worry

What The Chip: Intuitive Surgical closed 2025 with a victory lap—$2.87B in Q4 revenue (+19% YoY), 18% procedure growth, and $2.5B in free cash flow that nearly doubled the prior year. The company crossed 20 million patients treated since 1997, with the da Vinci 5 upgrade cycle accelerating as 303 systems shipped in Q4 (+74% YoY). But the champagne was flat when management guided 2026 procedure growth to just 13-15%, down sharply from Q4’s 18% exit rate. The culprit: a laundry list of macro concerns from ACA subsidy uncertainty to “intensified” Chinese competition. Investors now face a classic setup—does the da Vinci 5 cycle and new ASC strategy overcome external headwinds, or is the deceleration structural?

Details:

🏥 Milestone Achievement: Intuitive has now treated over 20 million patients with 3.1 million procedures performed in 2025 alone. This validates robotic surgery’s transition from niche innovation to mainstream standard of care across multiple procedure types.

📈 da Vinci 5 Momentum: 303 systems placed in Q4 (+74% YoY) with 146 trade-ins (+135% YoY) as hospitals aggressively upgrade their fleets. The installed base hit 1,232 systems being used by 10,000+ surgeons. The upgrade cycle is just beginning at 11% penetration of eligible systems.

💰 Cash Generation Inflection: Free cash flow hit $2.5B for 2025 (+92% YoY), funding $2.3B in share buybacks at an average price of $478/share while growing cash to $9B. The business model is inflecting from growth investment to cash return mode.

🛡️ Margin Resilience: Pro forma operating margin expanded 70bps to 37% for full year despite absorbing 95bps of tariff headwinds. This demonstrates pricing power and operating leverage—management guided to 120bps of tariff impact in 2026 yet margins should still hold.

🚩 China Competition Intensifies: Management explicitly stated “robotic competition in China intensified in Q4” with provincial tenders showing preference for local suppliers and lower pricing impacting win rates. This is the first time Intuitive has acknowledged material competitive pressure in China.

🔮 ASC Strategy Unveiled: The XiR system is positioned as a “sizable long-term opportunity” for ambulatory surgery centers, with 70% of the ASC opportunity coming from facilities already affiliated with Intuitive’s IDN customers. This leverages existing relationships to unlock a new market segment.

⚡ After-Hours Surge: Emergency procedures (cholecystectomy, appendectomy) grew 35% YoY—the fastest growth in any procedure category. This indicates robotic surgery is penetrating acute care settings, not just scheduled elective procedures, expanding the addressable market.

📦 Ion Platform Accelerating: Ion lung biopsy procedures grew 44% YoY with the installed base approaching 1,000 systems. Management enhanced disclosure around Ion metrics, signaling confidence this becomes a meaningful growth driver alongside

Youtube Channel - Jose Najarro Stocks

X Account - @_Josenajarro

Join WhatTheChipHappened Community — 33% OFF Annual Use Code “2026”

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

Disclaimer: This article is intended for educational and informational purposes only and should not be construed as investment advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.