The Memory Shortage Nobody Can Fix

Why the most powerful buyer in tech is begging to buy Chinese chips, why China might say no, and why the panic around Micron is pointed the wrong way

Apple just raised prices on the MacBook and the iPad by 20%. The reason it gave was neither tariffs nor a redesign. It was memory!

DRAM prices have climbed so hard that, according to Financial Times reporting, Apple is now lobbying the Trump administration for cover to buy DRAM from CXMT, China’s national champion in memory and a company that sits on the Pentagon’s military blacklist.

That is the headline everyone has. Below it sit three things almost no one is connecting, and together they flip the story. The US government faces a real dilemma. China’s government may block the deal anyway. And even if everything lines up, a wafer math problem means it does not fix the shortage that started all of this. Here is the full picture of the chip is happening!

What actually happened

Apple approached the Commerce Department more than a month ago. The request is for political cover, not a legal exemption, because Apple is not breaking any law. CXMT sits on the Pentagon’s 1260H list, which flags suspected military ties but does not block commercial deals. The list that would block a deal is the Commerce Department’s Entity List, and CXMT is not on it.

So why ask permission at all? Because Apple has been burned here before. In 2022 it neared a deal to buy NAND from YMTC for iPhones sold in China and walked away after a bipartisan backlash, including a letter from then-Senator Marco Rubio. Rubio is now Secretary of State. The politics are worse this time, not better.

A quick note before the rest of this. If you want to go deeper than the free posts, the community is where the real work lives. Multiple exclusive live streams every week. Earnings deep dives. The AI apps I build for research. Numerous conference coverage, and more are added all the time. You can join at [whatthechiphappened.com].

The administration’s impossible choice

This is a genuine fork, and both directions hurt.

Allowing the deal helps on inflation. Memory sits in phones, laptops, cars, and data centers, so a 60-plus percent jump in DRAM flows straight into consumer prices and into the inflation print. A White House that wants to show progress on inflation has a direct incentive to let cheaper Chinese memory cool things off. Apple raising consumer prices by 20% and blaming memory is the kind of headline an administration does not want to see repeated.

Blocking the deal protects the strategy. Five years of US chip policy has aimed to slow China and protect domestic and allied producers. Micron (MU) is the American champion. Samsung and SK Hynix are South Korean allies. Greenlighting Apple to buy from a blacklisted Chinese DRAM maker would hand China’s national champion the most valuable customer reference on Earth. Once Apple validates CXMT, every other phone and PC maker feels safe following.

There is no clean answer. Tame inflation and prop up a rival, or protect the rival’s competitors and swallow higher prices into a sensitive economy.

Would China even allow it?

Here is the angle the coverage is missing. We keep assuming this is Washington’s call. Beijing gets a vote, and Beijing has reason to say no.

If CXMT ships large DRAM volume to Apple, that is China spending scarce memory capacity to relieve a US shortage. Memory is a bottleneck for AI buildout, so easing it in America makes it easier to build AI systems in America. From Beijing’s seat, that reads as a strategic gift.

We are not guessing, because this has already happened twice. When the administration re-allowed NVIDIA (NVDA) H20 sales to China in 2025, Chinese regulators told ByteDance, Alibaba, and Tencent to avoid the chip on security grounds, and NVIDIA ended up halting H20 production. When the more powerful H200 was approved for export in December 2025, the Commerce Secretary later admitted NVIDIA still had not sold any into China, because Beijing was steering demand to domestic players. Twice, Washington opened a door and Beijing refused to walk through it.

Flip that onto memory. If Beijing turned down American chips it wanted in order to build its own, why would it let CXMT spend scarce capacity bailing out Apple and cooling American inflation? China can frame an Apple deal as exactly the giveaway it just spent two years refusing.

The wafer math that breaks every easy fix

Now assume Washington says yes and Beijing says yes. It still does not fix the shortage, and this is the most important concept in the whole story.

It is called the HBM trade ratio. High bandwidth memory, the stacked memory that sits beside AI accelerators, consumes roughly three times the wafer capacity of standard DDR5 per gigabyte. Picture a fab as a kitchen with a fixed number of burners. Regular DRAM is a one-burner dish. HBM is a three-burner dish serving the same number of people, because of die stacking, lower yields, and slower packaging. Every burner shifted to HBM removes three burners of commodity supply, not one.

Add the economics. Revenue per wafer for HBM runs three to five times higher than DDR5, so makers race to convert, and every conversion pulls triple its weight out of the standard memory pool that feeds phones and laptops. Micron says the HBM ramp and its trade ratio are directly constraining non-HBM DRAM supply.

CXMT and YMTC do not make competitive HBM. So even a flood of Chinese-standard DRAM adds supply to the tier that matters least to AI-driven tightness, while the leading edge stays starved. New fabs do not deliver meaningful output until fiscal 2028. The Apple-CXMT drama is happening one floor below where the real squeeze lives.

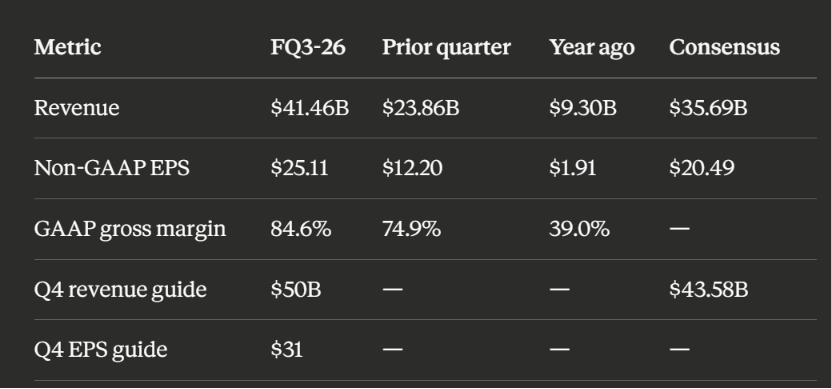

What Micron just told us

Micron reported fiscal Q3 2026 on June 24, and the numbers argue against the panic.

Revenue beat by 16%. EPS beat by twenty-two and a half percent. The forward guide came in roughly $6 billion above Street models, with EPS guided to a record. Demand is contracted, not hoped for. Micron disclosed strategic customer agreements with about $22 billion in total commitments, including roughly $18 billion in cash deposits already on the balance sheet, at floor-price margins management says exceed any prior peak.

Why the mobile scare is backwards

Micron’s mobile bit shipments have fallen for three consecutive quarters, creating a massive bearish thesis. That reading is backward.

Mobile bits are down because Micron is moving those wafers to data center, where the trade ratio and the margins make each one worth multiples more. The earnings preview reporting confirms it plainly: supply allocation toward higher-margin data center customers is what is constraining mobile and PC bit shipments. Micron is not losing the burners. It is walking its own burners to the dish that pays five times as much.

The severity stat seals it. On the previous earnings call, CEO Sanjay Mehrotra said Micron can meet only about “50% to two-thirds” of demand from several key customers in the medium term. A supplier turning away a third to a half of its biggest customers’ orders is not losing a volume fight. Shipping fewer mobile bits is a choice about where scarce wafers go, and right now they go to the AI data center.

What it means for investors

The setup is two things at once, and keeping them separate is the whole game.

Sentiment will be loud and negative on fear days. Micron is up roughly 700 percent over the past year, past a trillion in market cap, so it will whip on any China headline, and the CXMT story hands bears a clean narrative to attach to every red candle. That volatility is real and worth bracing for.

Fundamentals point the other way. A net cash balance sheet, return on equity near forty percent, 18 billion dollars of customer deposits in hand, a forward quarter guided six billion above consensus, and a shortage that physics keeps tight until 2028. When the actual prints land, the demand is contracted and visible enough that they are set up to be strong.

To be clear, I am not a Micron shareholder, so this is not a recommendation. It is a reminder to separate the noise from the math. Watch two things from here. Whether Commerce signals anything to Apple, and whether Beijing makes a sound about CXMT exporting to a US customer. The second will tell you more than the first.