WHEN A MASSIVE BUYER BLINKS ON MEMORY

Apple is raising prices because of memory. That tells you more about the shortage than any spot price ever could.

On June 17, Tim Cook told the Wall Street Journal that Apple (AAPL) will raise prices across iPhone, iPad, and Mac to offset surging memory and storage costs. He called the increases “unavoidable” and said “the situation has become unsustainable.” He compared the memory shortage to a hundred-year flood.

For a company that treats price stability as a religion, that is a remarkable thing to say out loud. And the reason it matters has very little to do with Apple’s product roadmap. It has everything to do with what Apple’s surrender signals about the memory market.

Why this is the real signal

Apple is one of the largest memory buyers on the planet. Scale like that is supposed to be a shield. Long-term supply agreements, priority allocation, and a balance sheet measured in hundreds of billions normally let Apple absorb component swings that flatten smaller hardware makers.

This time the shield did not hold.

When the most powerful buyer in consumer electronics decides it can no longer eat the cost, the takeaway is not about one company’s margins. It is about how tight the underlying market has become. Two details make Cook’s move more telling than a routine price bump. Apple hates raising prices, especially when it expects relief soon, so a company that thought pricing would normalize in a quarter or two would simply carry the cost and wait. Cook is not waiting. He also confirmed Apple is “willing to use our balance sheet” to help secure supply, while ruling out building its own memory factories. You do not spend cash on a problem you believe clears on its own.

Apple told us this was coming

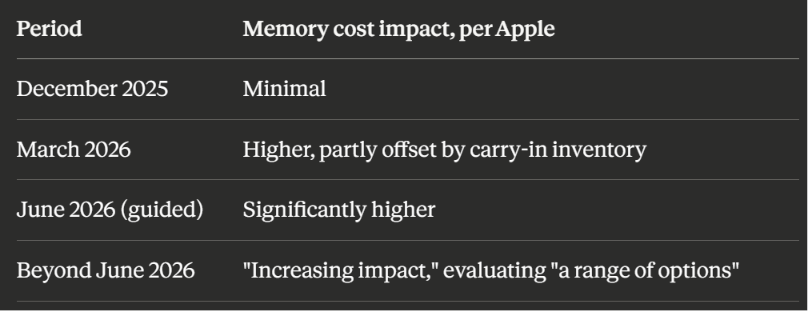

The June interview did not arrive out of nowhere. On Apple’s April 30 fiscal Q2 call, Cook walked analysts through a memory-cost trajectory that got worse at every step.

That last row is the one that mattered. Cook said memory costs would “drive an increasing impact” on the business beyond June, and that Apple would “look at a range of options.” Six weeks later, the WSJ interview showed what that phrase meant. The escalation was telegraphed in plain sight.

CFO Kevan Parekh put a figure on the early damage. Product gross margin fell 200 basis points sequentially in the March quarter, driven in part by higher memory costs. That was before the “significantly higher” June quarter, and before the “increasing impact” beyond it.

The supply side says this runs long

None of this resolves quickly, because the squeeze is structural, not cyclical.

At the J.P. Morgan technology conference on May 20, Micron (MU) EVP of Global Operations Manish Bhatia said demand keeps outpacing the industry’s ability to supply, and that tightness across HBM, DRAM, and NAND will continue “well beyond calendar year 2026.” Each new technology node now adds less bit growth than the last. The shift toward high-bandwidth memory for AI servers makes it worse, because HBM die are larger and it takes more than three times as many wafers to deliver the same number of bits. Every wafer pulled toward HBM is a wafer that is not producing the commodity DRAM that goes into a phone.

Micron’s pricing language has hardened to match. On its March post-earnings call, CFO Mark Murphy said both DRAM and NAND pricing was “up strongly,” with NAND up even more than DRAM, and guided that price would again be the largest growth factor the following quarter. Chief Business Officer Sumit Sadana was blunter on duration, saying Micron does not yet have a high-confidence view of when supply will catch up with demand. New greenfield capacity from projects like Idaho and the acquired Tongluo fab in Taiwan does not deliver meaningful output until fiscal 2028. The timeline itself tells you what kind of problem this is.

There is one more number that frames Apple’s bind. Micron has noted that key customers can secure only 50% to two-thirds of their bit demand in the medium term. Even priority buyers are being rationed. Cook saying “unsustainable” and Sadana saying supply has no clear catch-up date are the same fact read from opposite ends of the invoice.

A read from outside the chip world

The cleanest confirmation comes from a company with no stake in either side of the argument. ATRenew (RERE), China’s largest pre-owned electronics platform, told investors on its Q4 2025 call in March that as memory prices climbed, Android makers were forced to raise new-device prices while Apple held its pricing relatively stable. Management said that widening gap “reinforced Apple’s position in the pre-owned market,” and that Apple’s share of its own business rose as a result.

That is the whole arc in one data point. Apple’s scale bought it time to hold the line while rivals moved first. The April call and the June interview are the sound of that buffer finally running out.

What it means for investors

Pricing power has shifted from the device makers to the memory suppliers, and the supply side says it stays there past 2026. That favors the makers, primarily Micron (MU), SK Hynix, and Samsung, and it pressures gross margins at memory-heavy hardware companies that cannot fully pass the cost through.

Apple can pass through more than most, thanks to brand strength and an iPhone cycle running at 99% U.S. customer satisfaction. Thinner-margin PC and Android builders have far less room, which is why several of them moved on pricing before Apple did. The gap between who controls the supply and who consumes it is the story to track from here. Two near-term checkpoints will tell you which way it breaks: Micron’s next earnings print and its commentary on pricing, and whether Apple leans on higher-storage tiers rather than headline price hikes to protect the optics while still expanding margin per unit.

Bottom line

When the biggest buyer in the room says it can no longer absorb memory costs and starts spending cash to secure supply, that is not a complaint. It is a signal that the shortage runs deep and runs long. The memory cycle has been called dead more than once. The companies actually writing the checks are telling you it is very much alive.

If this is how you like to read the market, the rest is inside.

Most of the research I do never makes it to the free list. The full earnings and conference breakdowns, the companies I am tracking across chips, memory, equipment, and AI infrastructure, and the analysis I use to make my own decisions all live in the What The Chip Happened community. It is built for people who take semiconductor investing seriously and want the work done.

Join here: whatthechiphappened.com

Sources: Tim Cook interview, Wall Street Journal, June 17, 2026. Apple fiscal Q2 2026 earnings call, April 30, 2026. Micron fiscal Q2 2026 post-earnings call, March 18, 2026, and J.P. Morgan Technology Conference, May 20, 2026. ATRenew fiscal Q4 2025 earnings call, March 11, 2026.